Options Matter

How Optionality Has Become a Core NBA Currency

Overview

In a league governed by a Hard Cap system, control and flexibility are vital. In certain ways, this era of the NBA is defined by 2nd Apron restrictions, trade aggregation limits, and increasingly punitive Tax mechanics. Optionality has consequently become one of the most valuable forms of currency a Front Office can possess. How every dollar is allocated now carries heightened strategic consequences. What was once a simple calculus of valuation, term, and AAV has become a far more exacting exercise in risk management. Contracts are scrutinized not only for a player’s current value, but also for how that commitment shapes future flexibility, trade optionality, and the ability to respond to unforeseen outcomes. This recalibration has not been confined to marquee negotiations. Every tier of the market, from Stars to minimum signings, has felt the effects of this more constrained financial ecosystem. And, in this environment, negotiations have taken on a noticeably harder edge, with teams far less willing to concede structural leverage at the margins.

It is in this context that option years, both Player Options (PO) and Team Options (TO), have grown in strategic importance. Option years can determine who controls the choice to extend or end a deal, effectively allocating risk and upside between player and team. The presence or absence of an option year can dictate not only negotiation leverage but also trade value, roster construction, and long-term strategic optionality. Understanding how teams and players deploy these tools has become essential for interpreting both the league’s financial and roster-building landscapes.

The Hidden Value of Options

At a surface level, option years determine who controls the final decision point of a contract and where the balance of risk ultimately sits. A PO allows the player to maintain more leverage and hold more favorable outcomes while insulating against downside. Whereas a TO provides the franchise with that same protection and the ability to walk away from deals that might no longer fit the Cap Sheet architecture. In an environment where mistakes are increasingly difficult to unwind, particularly for teams operating near the Tax and/or Aprons, that allocation of risk has become one of the most consequential structural decisions embedded within modern NBA contracts.

While the decision to exercise or decline an option is consequential in its own right, one can argue that the true significance of the provision can often be traced back years earlier to the moment the contract is negotiated. The inclusion and structure of an option year can reveal a great deal about a team’s broader roster-building strategies, anticipated financial inflection points, and the mechanisms put in place to either preserve flexibility or create potential exits down the line. At the same time, options can also serve as a window into the negotiation itself, as in whether a player accepted a lower salary in exchange for greater future optionality, or whether a franchise was willing to grant that flexibility as a reflection of how highly it values the player within its long-term plans.

For example, a single option at surface value might not appear to carry much weight; however, when layered together with other mechanisms (including without limitation, short-term deals, partial guarantees, other options, or carefully timed extensions), it can create meaningful outs for a franchise. These structures allow a team to open multiple pathways with a single set of decisions, preserving flexibility and optionality that extends beyond any individual contract. Over several offseasons, certain outs can accumulate or be sequenced and structured to give Front Offices maneuverability that is not immediately visible on the salary sheet.

Viewed through this lens, both POs and TOs are far more than contractual footnotes. In this CBA environment they have become signals of organizational philosophy. Examining how these options are distributed across the league reveals, among other things, which teams prioritize flexibility, which ones are willing to allocate risk to players, and how franchises layer these mechanisms to manage roster construction over multiple seasons.

To ground these concepts in concrete numbers, the following dataset examines the current distribution of POs and TOs across non-rookie contracts.

The Numbers

To illustrate how POs and TOs operate across the league, I have compiled a dataset listing the current distribution of non-rookie contracts containing options. This breakdown highlights how leverage shifts between players and teams depending on salary tier, role, and market context, revealing the structural patterns that guide negotiation dynamics. Overall, there are currently 53 non-rookie contracts that contain a TO, and 68 contracts that contain a PO.

At the surface level, these numbers suggest that POs remain more prevalent than TOs. However, the distribution is far from uniform. Different salary bands, positional roles, and team contexts reveal distinct patterns in how options are allocated. Examining these patterns can reveal not only who holds structural control, but also how teams strategically deploy options to manage risk, preserve flexibility, and shape potential trade and extension scenarios over multiple seasons.

The following subsections dive deeper into the data, highlighting key insights and patterns in how options are distributed and deployed across the league. All figures presented reflect the current set of active PO and TOs. Deals in which an option has already been exercised or declined are not included in the reviewed data.

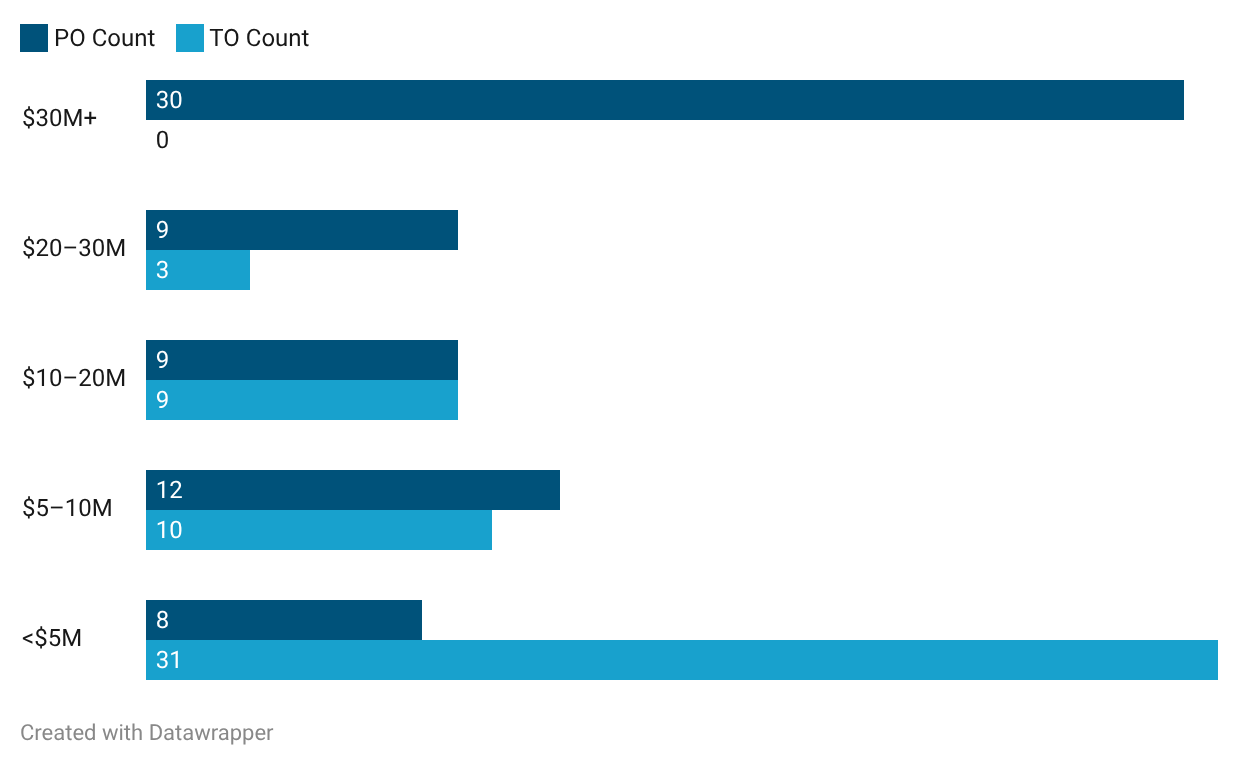

Option Allocation - AAV Tiers

Insights and Observations:

Player leverage is effectively absolute at the top of the market. Every contract above $30M AAV that includes an option is a PO, underscoring how the league’s highest-tier players maintain structural control over the final years of their deals.

Negotiating leverage begins to shift slightly below this $30M tier. In the $20–30M range, POs still dominate (75%); however, TOs begin to appear, suggesting teams gain modest structural protection once salaries fall outside the elite tier.

The $10–20M band represents the league’s clearest negotiation equilibrium. With POs and TOs split evenly, this tier appears to be where leverage between players and teams is most balanced, reflecting the push-and-pull typical of mid-tier contract negotiations.

Mid-level rotation players still secure meaningful optionality. Even in the $5–10M range, POs slightly outnumber TOs, indicating that many established rotation players retain enough leverage to negotiate future flexibility.

Team control becomes dominant at the bottom of the market. Among contracts below $5M AAV, TOs account for 79% of all options, reflecting how franchises prioritize downside protection and roster flexibility when dealing with minimum or developmental contracts. This AAV bracket also accounts for 58% of all TOs, highlighting how heavily TOs are concentrated in the lower salary tiers, in contrast to POs, which skew toward higher brackets.

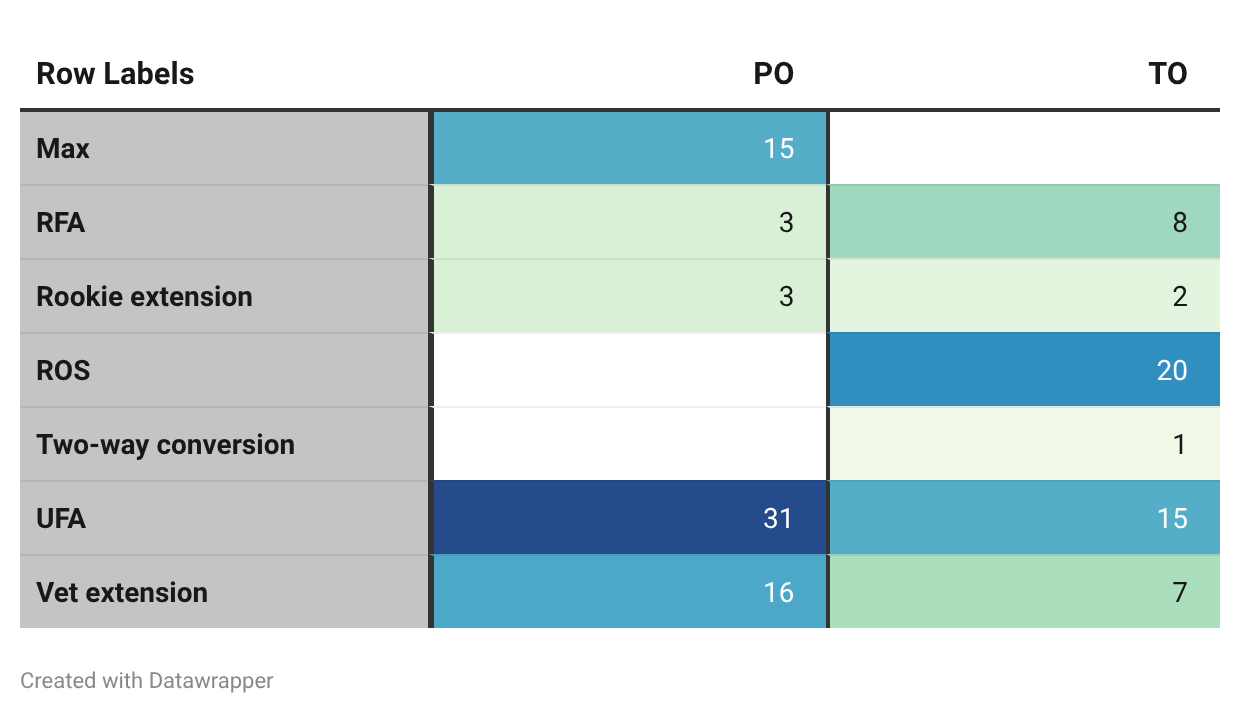

Option Allocation - Signing Mechanisms Utilized

Insights and Observations:

Team control is concentrated in short-term and low-commitment pathways. Rest-of-season deals and Two-Way conversions account for 21 TOs and zero POs, illustrating how teams preserve maximum flexibility when operating in evaluation or non-guaranteed roster contexts. Of the 8 TOs handed out to RFAs, most fell into the lowest AAV bucket (under $5M), reinforcing that low-commitment deals tend to favor the team, which holds greater leverage in these negotiations.

Compressed financial dynamics and the scarcity of Cap Space in UFA are driving a clear tradeoff between salary and optionality. As teams prioritize flexibility and negotiate from a hardline stance, players are increasingly conceding on AAV in exchange for structural leverage, using POs as a substitute for lost upside. Recent examples (such as Fred VanVleet, Kyrie Irving, James Harden, and Julius Randle) illustrate this shift, pairing lower AAVs relative to prior earnings with the ability to re-enter the market and recapture value under more favorable conditions.

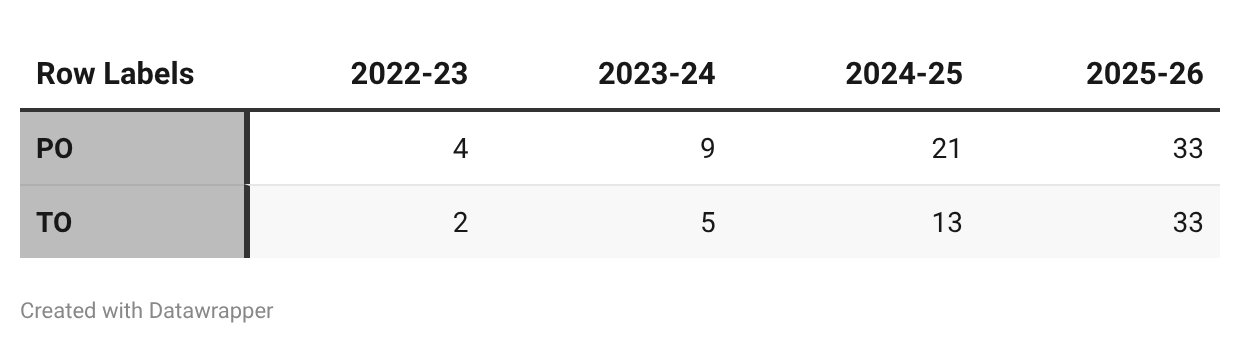

Option Allocation - Year Contract Signed

Insights and Observations:

Both POs and TOs have surged in recent signing classes, but for different reasons. TOs have risen as a tool for protection and roster flexibility, while POs have spiked, most notably in 2025–26, reflecting a parallel increase in players prioritizing optionality in a more constrained financial environment.

UFA has become the primary arena for option-based negotiation. The sharp rise to 33 POs and 26 TOs in 2025–26 UFA deals demonstrates that both sides are increasingly negotiating around structure (not just salary) with optionality serving as a key tradeoff variable. This also reflects how POs tend to outpace TOs in the offseason, while in-season mechanisms (rest of season deals and conversions) rebalance the totals.

As stated earlier, the figures reflect only currently active POs and TOs. Options that have already been exercised or declined are excluded. This may help explain why POs outnumber TOs in past seasons. Deals with POs are more likely to “last” on the books, whereas TOs are concentrated in lower-salary contracts. These lower salary contracts tend to be shorter-term (the average term for a TO deal is 2.98 years, compared with 3.37 years for a PO deal), and more likely to be renegotiated or cut short before their term ends. This, in turn, leads to natural attrition that reduces their presence in the live dataset. Additionally, if the Bucks’ eight POs from the 2025 offseason are excluded, the average term for PO deals rises to 3.5 years, highlighting how a small number of short-term outliers can meaningfully affect averages.

Max Contracts

Insights and Observations:

Elite players retain full structural leverage at the top of the market. Among the 15 max contracts in the NBA that contain an option year, all feature a PO. This reinforces how the league’s highest-tier players consistently maintain control over the final decision point of their deals.

The option year functions as a built-in leverage reset. By preserving the ability to re-enter Free Agency before the contract fully expires, POs on max deals allow stars to continually reassess market conditions, enabling them to renegotiate from a position of strength and maintain long-term control over their contractual and career trajectories.

Option Allocation - Organizational Breakdown

Context is critical when analyzing how teams deploy options. The timing, frequency, and structure of these options depend not just on salary tier or player role, but also on each franchise’s broader strategy, roster construction goals, and future financial constraints. That said, patterns in TO and PO usage can reveal a great deal about what Front Offices value, which positions or players they prioritize, how they manage risk versus flexibility, and how they sequence contracts to maintain optionality across multiple seasons. Even without seeing the full strategic plan, careful observation of option deployment provides a window into the organizational philosophy guiding a team’s decision-making and priorities. In that sense, option deployment can also signal how a team views its place on the league landscape.

Regarding option usage, in the league right now there are two extremes: the Milwaukee Bucks and the Oklahoma City Thunder. The Bucks handed out an astounding eight POs this past offseason. This outcome was largely driven by team context, as the Front Office faced pressure to construct a competitive roster around Giannis Antetokounmpo and reinforce organizational commitment to contention. In that environment, POs functioned as an additional incentive in negotiations, helping the Bucks secure talent across multiple pathways, including extensions and Free Agent signings.

The Thunder has taken the opposite approach, making TOs a core principle within their roster-building strategy (a philosophy that I have written about extensively). The Thunder consistently emphasizes team control across its books. Of the last eight non-max contracts the organization has signed (among players still on the roster), seven include a TO. This approach extends across its Cap Sheet, with TOs in place to either exercise or decline in every offseason through 2028–29. These built-in decision points provide a layer of structural flexibility, allowing the organization to offset Max-driven financial compression while maintaining the ability to pivot at key inflection points. In some cases, these contracts and extensions may have appeared as overpays or even risky at the time of signing. However, that risk can be mitigated or justified by the added layer of team control, as a TO preserves an exit if the deal does not age well while retaining upside if it does.

Tradeoffs and Tactical Leverage

From a straight value perspective, the presence of an option can materially alter the range of outcomes attached to a contract. The direction of that impact depends not only on the type of option, but also on team context. For high-salary teams operating near or above the Tax and/or Aprons, the downside risk associated with a PO becomes significantly more pronounced. If a player underperforms relative to his contract, the presence of a PO adds an additional layer of constraint, as the player is incentivized to opt in, making the contract more difficult to move and effectively locking in that salary slot.

The impact of POs on trade value is highly context-dependent, often functioning as either a constraint or a source of flexibility depending on team circumstances.

Let’s consider Zeke Nnaji and the Denver Nuggets as an example. Nnaji has fallen out of the rotation on a team that has, at times, operated above both the Tax and Apron thresholds. His $8M AAV already presents challenges as it functions as a near “dead” salary slot. When factoring in the PO in the final year of the deal, the contract becomes even more difficult to move, increasing the likelihood that the salary remains on the books and, in turn, placing greater pressure on the rest of the roster to deliver value commensurate with each player’s respective Cap hit.

A similar dynamic was observed with the New York Knicks and Guerschon Yabusele. Despite the relatively modest size of the contract (2-years $11M), the inclusion of a PO materially impacted its tradability. Given the Knicks’ financial positioning and contending status, maximizing each salary slot was critical. Yabusele’s underwhelming play led the team to explore trade scenarios less than six months after signing him; however, the presence of the PO significantly limited the market. This illustrates how even smaller deals can become disproportionately restrictive when paired with certain types of optionality. Ultimately, Yabusele waived his PO to facilitate a trade to Chicago, underscoring the sensitivity of trade value to option structure and the degree to which optionality can dictate transaction outcomes.

However, there is a flipside to the option–trade value dynamic. The most straightforward benefit of options in trades comes when a team acquires a player with a TO, gaining the ability to unilaterally create Cap relief or open a roster spot. It is important to note, however, that the value of options in trade scenarios extends beyond that binary outcome.

In certain cases, POs can function as a bridge to flexibility rather than as a constraint. Consider the Minnesota Timberwolves when they acquired Julius Randle. Minnesota was facing an increasingly untenable financial outlook and 2nd Apron future. In moving Karl-Anthony Towns (who had multiple years remaining on his contract) for Randle, the team effectively exchanged long-term, fixed salary for a more flexible slot.

Randle’s PO introduced a layer of variability that Towns’ deal did not have, creating the potential for the contract to function as an expiring salary slot. When Randle ultimately declined the option and signed an extension at a lower number, it allowed the Timberwolves to rework their Cap Sheet and create breathing room below the 2nd Apron. This illustrates how, in the right context, a PO can carry positive trade value. This is not because a PO guarantees flexibility or gives an organization leverage, but because it introduces pathways that would not otherwise exist.

This logic may also help explain why the Cavaliers traded for Harden, as the PO introduces a pathway to renegotiate the contract downward via an opt-out, helping the team navigate 2nd Apron constraints while still offering the player long-term security. Harden’s contractual situation stands in stark contrast to that of Darius Garland, who still had two years remaining on his deal and therefore did not offer the same near-term opportunity to rework salary.

Final Points to Consider

In today’s NBA landscape with punitive Tax and Apron thresholds and limited avenues for roster flexibility, the relative scarcity of TOs on non-rookie deals (particularly those that are not rest-of-season deals) is notable. Teams may be prioritizing immediate cost savings over structural control. And yet, TOs offer a powerful mechanism to manage future financial and roster risk, creating clean exit points and preserving maneuverability in an increasingly constrained environment. This suggests that TOs may be underutilized relative to their potential value in this constrained landscape.

Conversely, POs remain a double-edged sword. While they expose teams to downside if a deal underperforms, they also introduce strategic optionality, allowing players to opt out, re-enter the market, or renegotiate. This provides a form of flexibility for teams that can be leveraged to navigate tight Cap situations. Together, these patterns underscore how optionality, alongside salary, has become a central currency in modern NBA roster and financial strategy.

Great read

Where do the Knicks fall in the spectrum of TO vs PO relative to others teams?